Retirement Series: Traditional Savings Account

Turnkey Rental Investment vs. The Traditional Retirement Plan: Savings Accounts

This article is the third installment in a series on retirement plans. In each post, I compare paper asset options against turnkey real estate investments. My goal is to show you why you may be better off calling your turnkey provider than your banker.

Unlike 401(k)s and Individual Retirement Accounts, savings accounts are sometimes used as a method of stashing away funds for retirement, trips, or emergency funds. The misconception oftentimes is that a savings account is a form of investment. Comparing real estate investment and savings accounts can be correlated to the old adage of comparing apples and oranges, they differ more than they're similar.

Rental income gives you more freedom to invest and reinvest on your own terms, and its often cheaper and easier to access your capital in a rental investment than in one of the aforementioned retirement investments.

If your goal is to save money, than a savings account is an effective way to stash away money, plan for a vacation, or create an emergency fund.

How does a Savings Account work?

For this article, I'll briefly talk about three types of savings arrangements:

Savings Account - This is the most basic type of savings account you can open with your traditional bank. Per the FDIC, the average interest rate currently being offered is 0.06%.

Money Market Account - This account is similar to a regular savings account, only it'll require a much higher minimum balance than your typical bank account. Typical money market accounts are currently returning 0.8% per year.

Certificate of Deposit (CD) Account - With a CD, you agree to deposit your money into an account for a fixed amount of time for a fixed return. The best rates current available per Bankrate.com are 1.3% on a 1 year CD and 2.25% on a 5 year CD with no minimum contribution. Early withdrawals, of course, face a stiff penalty.

What are the advantages of Savings Accounts?

The primary benefit of an institutional savings account is safety. Not only will your funds be secure with the bank than in the stock market, but they'll also be insured by the FDIC. While you may not get much of a return on your deposit, you know your funds won't disappear on you.

Since your savings are made with after-tax dollars, Uncle Sam has no say over what you do with your savings account or when you do it. Unless your money is in a CD, it can be liquidated at anytime and made available to you with no penalties or taxes for withdrawal.

What are the disadvantages of a Savings Account?

When it comes to protecting your hard-earned money, safety is important. However, so is risk mitigation. Even so, there is such a thing as playing it too safe. A savings account is NOT a viable option for investing. Despite the interest you may earn on any one of the preceding savings options, the annual rate of inflation most often exceeds the interest you earn on the money you have sitting in a savings account. If your objective is to invest money and plan for retirement, real estate investment is a low risk option that should be considered.

Let’s say, at age 25, you begin socking away $5,500 a year in savings. After 40 years and $220,000 of initial investment at a rate of 1.3%, you can expect to gain a slim $286,169. If you hope to live 20 years hence, that’ll give you about $14,000 a year.

Would that be enough for you to live on today? How about after 40 years of inflation?

How can turnkey rental property be a better long-term investment?

People who tend to favor “safe” options like the savings account do so because they’re afraid of the risk associated with investment options, especially those having to do with real estate. What some seem to forget is that you can lose money with a savings account. The Federal Reserve has determined that an annual increase of 2 percent is most effective for balancing price stability and maximizing employment (https://www.federalreserve.gov/faqs/economy_14400.htm).

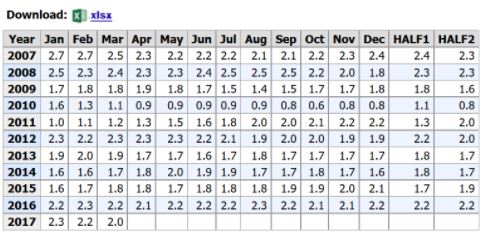

Below is a graph by the Bureau of Labor Statistics recently composed showing the annual rate of inflation for the last ten years:

(https://data.bls.gov/timeseries/CUUR0000SA0L1E?output_view=pct_12mths)

Conclusion

Savings accounts are not investment accounts. Each has a different purpose. Savings accounts are for holding cash (or near cash) to cover emergencies, planned events like vacations and for eliminating market risk once you have achieved your investment goals and are ready to retire. However, if multiplying your funds is your objective, a savings account is not an option that should even be considered. If your goals are to increase income and net worth growth in a controlled (low risk) manner, consider turnkey real estate investing.